Auditing Dissertation Topics for 2026

Questions Students Are Asking About Auditing Dissertation Topics

The following questions have been gathered from student forums, academic discussion boards, and online communities where students regularly seek guidance on choosing their dissertation topics.

- What are the most relevant auditing dissertation topics for 2026?

- How do I choose a dissertation topic in auditing that is academic enough for a master’s level?

- Are there easy auditing dissertation topics for undergraduates that still meet university standards?

- What are the trending auditing dissertation topics for 2026 in areas like forensic auditing or corporate governance?

- Can I get auditing dissertation topics with examples that show me how to write a research aim?

- How do internal controls and audit quality relate to dissertation research?

- Where can I find auditing dissertation help if I get stuck during the writing process?

Why Choosing the Right Auditing Dissertation Topic Matters

Choosing the right dissertation topic in auditing is one of the most important academic decisions you will make. The topic you select shapes your research methodology, determines the sources you can access, and signals to your examiners how well you understand the discipline.

Auditing is a field that sits at the intersection of finance, law, ethics, and organisational behaviour. In 2026, it is evolving rapidly due to regulatory changes, digital transformation, and growing demands for transparency. This means students have a genuine opportunity to contribute fresh, meaningful research to a field that society urgently needs.

A well-chosen topic helps you stay motivated throughout the process. It also makes your research proposal stronger and your final submission more persuasive. Whether you are an undergraduate selecting your first dissertation topic or a PhD candidate developing an original contribution to knowledge, starting with the right research question changes everything.

If you have ever felt unsure where to begin, you are not alone. Many students benefit from online dissertation help at this early stage to clarify their direction before committing to a topic.

Download Auditing Dissertation Topics PDF

Students who want a personalised list of auditing dissertation topics curated by academic experts can access a downloadable PDF version of these topics. The PDF is made available after completing a short form, and it is designed to save time by matching topic suggestions to your academic level, area of interest, and research focus. Academic professionals review these lists to ensure they meet current university expectations and align with 2026 research standards.

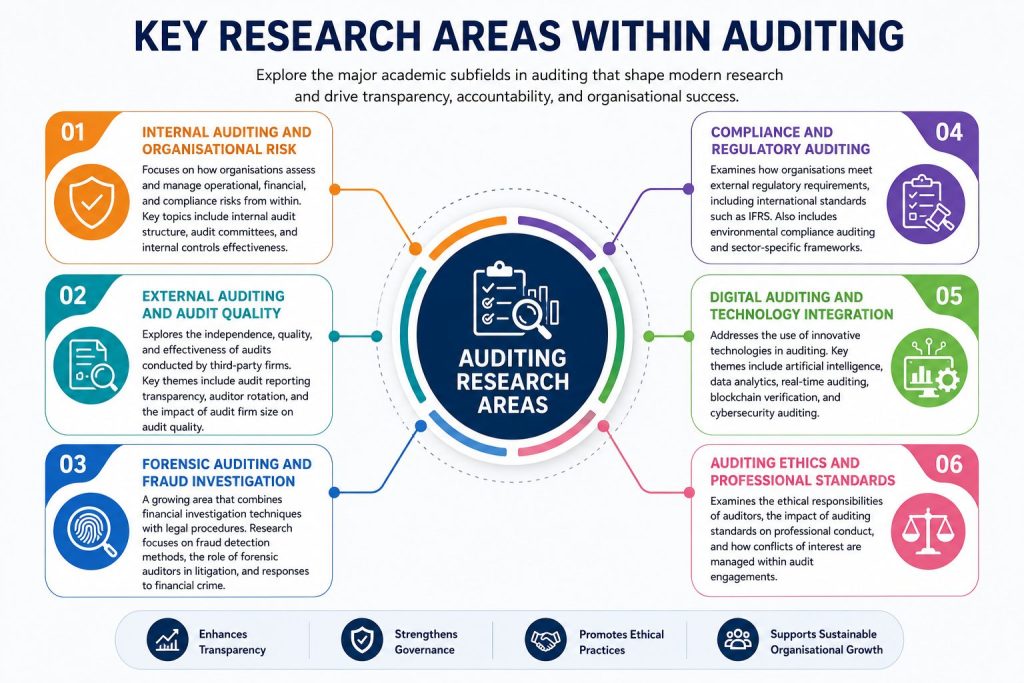

Key Research Areas Within Auditing

Auditing is a broad discipline with several well-established academic subfields. Before selecting a topic, it helps to understand the core research areas available to you.

Internal Auditing and Organisational Risk

Internal auditing focuses on how organisations assess and manage operational, financial, and compliance risks from within. Research in this area often examines how internal audit functions are structured, how audit committees operate, and how effectively internal controls prevent fraud or financial misstatement.

External Auditing and Audit Quality

External auditing research explores the independence, quality, and effectiveness of audits carried out by third-party firms. Key themes include audit reporting transparency, auditor rotation, and the impact of audit firm size on the quality of financial assurance.

Forensic Auditing and Fraud Investigation

Forensic auditing is a growing area that combines financial investigation techniques with legal procedures. Research topics here focus on fraud detection methods, the role of forensic auditors in litigation, and how organisations respond to financial crime.

Compliance and Regulatory Auditing

Compliance auditing research examines how organisations meet external regulatory requirements, including those set by international standards such as IFRS. This area also includes environmental compliance auditing and sector-specific regulatory frameworks.

Digital Auditing and Technology Integration

With artificial intelligence and data analytics transforming how audits are conducted, this subfield addresses the use of automated tools, real-time auditing, blockchain verification, and cybersecurity auditing.

Auditing Ethics and Professional Standards

This area examines the ethical responsibilities of auditors, the impact of auditing standards on professional conduct, and how conflicts of interest are managed within audit engagements.

Five Auditing Dissertation Topics With Examples

The following five examples illustrate how a research aim and supporting objectives are constructed for an auditing dissertation. These are designed to help you understand what a well-structured topic looks like at each academic level.

Example 1: Internal Controls and Financial Reporting Accuracy

Research Aim: To examine the effectiveness of internal controls in reducing financial reporting errors in publicly listed UK companies.

Objectives:

- To evaluate the relationship between internal control frameworks and reporting accuracy

- To identify gaps in current internal control practices across selected firms

- To recommend improvements to internal audit oversight processes

Example 2: Audit Quality and Firm Size in Emerging Markets

Research Aim: To investigate whether audit firm size influences audit quality in emerging economies.

Objectives:

- To compare audit quality indicators across Big Four and non-Big Four firms in selected emerging markets

- To assess how regulatory environments affect auditor independence

- To explore client perceptions of audit quality across firm categories

Example 3: Forensic Auditing in Corporate Fraud Detection

Research Aim: To assess the role of forensic auditing in detecting and preventing corporate fraud in the financial services sector.

Objectives:

- To review existing forensic auditing methodologies applied in fraud cases

- To analyse how forensic evidence is used in legal proceedings

- To determine barriers to effective forensic auditing in regulated industries

Example 4: Corporate Governance and External Audit Effectiveness

Research Aim: To explore the relationship between corporate governance structures and the effectiveness of external audits.

Objectives:

- To examine how board composition affects external auditor independence

- To assess the role of audit committees in strengthening governance mechanisms

- To evaluate how IFRS standards shape external auditor responsibilities

Example 5: Digitalisation and the Future of Compliance Auditing

Research Aim: To investigate how digital transformation is reshaping compliance auditing practices in UK financial institutions.

Objectives:

- To identify the digital tools currently used in compliance auditing

- To assess how technology adoption has changed auditor roles and responsibilities

- To propose a framework for integrating AI-based tools into compliance auditing workflows

80 Auditing Dissertation Topics for 2026

The following 80 topics are organised under key subfields within auditing. Each topic is narrow, researchable, and suitable for undergraduate, master’s, or PhD research. These represent some of the most contemporary auditing research topics available for 2026.

Internal Auditing and Organisational Risk

- The effectiveness of internal audit functions in managing operational risk in UK NHS trusts

- How audit committee independence influences internal audit outcomes in FTSE 100 companies

- The role of internal auditing in detecting early signs of organisational failure

- Internal audit maturity models and their application in small and medium enterprises

- The impact of internal auditing on reducing information asymmetry between management and stakeholders

- How risk-based internal auditing frameworks improve decision-making in local government authorities

- Evaluating the relationship between internal audit quality and corporate performance in listed firms

- Co-sourcing versus in-house internal auditing: implications for risk coverage in multinational firms

- How internal audit functions adapt to remote working environments in post-pandemic organisations

- The role of internal controls in preventing payroll fraud in public sector institutions

External Auditing and Audit Quality

- Does auditor rotation improve audit quality in European financial markets?

- The impact of audit firm tenure on the independence of external auditors in UK-listed companies

- Audit fees and their relationship to perceived audit quality in the banking sector

- How external auditors respond to management override of internal controls

- The effectiveness of going concern opinions as early warning mechanisms in corporate distress

- Non-audit services and auditor independence: evidence from mid-tier audit firms

- The influence of audit partner characteristics on audit report outcomes

- External auditor scepticism and its impact on the detection of earnings management

- How audit quality differs across industries in developed versus developing economies

- The reliability of audit reports in reflecting true financial health in the technology sector

Forensic Auditing and Fraud Investigation

- The effectiveness of forensic auditing techniques in uncovering procurement fraud in public institutions

- How forensic auditors contribute to anti-money laundering investigations in financial services

- The role of digital forensics in supporting financial crime prosecution

- Forensic auditing and its application in detecting fraudulent financial statements in SMEs

- How whistleblower policies interact with forensic audit investigations in large organisations

- The challenges of cross-border forensic auditing in multinational fraud cases

- Behavioural indicators of fraud risk and their incorporation into forensic audit methodologies

- Forensic auditing in the insurance industry: detecting false claims and policy abuse

- The use of data analytics in modern forensic auditing engagements

- How forensic audit findings influence corporate restructuring decisions after fraud discovery

Compliance and Regulatory Auditing

- The effectiveness of GDPR compliance auditing in UK financial services firms

- How environmental compliance auditing contributes to sustainability reporting in energy companies

- Regulatory auditing and its role in enforcing anti-bribery legislation in the construction sector

- The impact of IFRS adoption on external auditor responsibilities in emerging economies

- Tax compliance auditing and its effectiveness in reducing the shadow economy in developing countries

- How healthcare compliance auditing affects patient safety outcomes in NHS organisations

- The relationship between regulatory audit frequency and corporate misconduct in the banking sector

- Compliance auditing in the pharmaceutical industry: assessing adherence to clinical trial regulations

- How compliance auditors manage conflicts between regulatory requirements and client expectations

- The role of audit reporting in promoting accountability in government spending frameworks

Digital Auditing and Technology Integration

- The impact of artificial intelligence on the future of audit quality in professional services

- How blockchain technology is transforming audit evidence collection and verification

- Continuous auditing systems and their effectiveness in real-time risk monitoring

- The adoption of data analytics in external auditing: challenges and opportunities in the UK

- Cybersecurity auditing frameworks and their effectiveness in financial institutions

- How cloud computing introduces new risks and responsibilities for compliance auditors

- Robotic process automation in internal auditing: assessing efficiency gains and reliability

- The use of predictive analytics in identifying audit risks before engagement commencement

- How digital transformation affects auditor competencies and professional development requirements

- Algorithmic bias in AI-assisted auditing tools and its implications for audit objectivity

Corporate Governance and Auditing

- The relationship between board diversity and external audit effectiveness in FTSE 250 companies

- How audit committees influence the quality of financial disclosures in publicly listed firms

- Corporate governance failures and their connection to inadequate auditing practices

- The role of the audit committee chair in maintaining auditor independence

- Shareholder activism and its effect on audit committee accountability

- How integrated reporting affects the scope and methodology of external audits

- Corporate governance codes and their influence on auditing standards in developing economies

- The relationship between CEO power and auditor switching decisions in listed companies

- How family-owned businesses approach corporate governance and internal audit structures

- Audit quality in state-owned enterprises: the influence of government ownership on auditor independence

Auditing Ethics and Professional Standards

- The ethical responsibilities of auditors when clients engage in aggressive tax planning

- How auditing standards address conflicts of interest in audit engagements with related parties

- Professional scepticism and its decline in long-term auditor-client relationships

- The impact of ethical training on auditor judgment and decision-making quality

- How auditors balance commercial pressures with independence obligations in competitive markets

- Whistleblowing culture within audit firms and its effect on professional conduct

- The role of the Financial Reporting Council in maintaining auditing ethics in the UK

- Ethical challenges in audit engagements involving politically exposed persons

- How gender diversity within audit teams affects ethical sensitivity and fraud detection

- The influence of religious and cultural values on auditing ethics in Islamic finance contexts

Auditing in Specialised Sectors

- The effectiveness of auditing practices in the UK charity sector under current regulatory frameworks

- How public sector auditing contributes to accountability in local council spending

- Auditing challenges in the cryptocurrency and digital asset industry

- The role of social auditing in measuring non-financial performance in the retail sector

- Environmental, social, and governance auditing and its integration into traditional financial audits

- Auditing microfinance institutions in Sub-Saharan Africa: quality, access, and impact

- How auditing standards adapt to the unique risks of the fintech sector

- The effectiveness of value-for-money auditing in higher education institutions

- Auditing in the post-conflict reconstruction environment: accountability and transparency challenges

- How internal audit functions in the hospitality sector manage reputational and financial risk

How to Choose the Right Auditing Dissertation Topic for Your Level

Selecting a topic that matches your academic level is essential. At undergraduate level, you are expected to demonstrate a clear understanding of existing literature and apply it to a focused research question. Topics such as internal controls, audit quality, or compliance auditing work well at this level.

At master’s level, your dissertation should show critical analysis, methodological awareness, and the ability to connect theory with practice. Topics involving digital auditing, forensic methods, or corporate governance allow for this depth.

At PhD level, your research must make an original contribution to knowledge. Topics in auditing ethics, algorithmic bias in digital auditing, or the institutional factors shaping audit quality in developing economies are examples where genuine gaps in the literature exist.

If you are still unsure which level your topic suits, seeking dissertation support for auditing students from an academic advisor or writing specialist can help you assess the scope and feasibility of your research idea.

Tips for Developing a Strong Auditing Dissertation Proposal

Once you have a topic in mind, the next step is turning it into a convincing research proposal. Here are some practical steps:

- Narrow your focus early. A topic like “auditing and corporate governance” is too broad. A topic like “the impact of audit committee independence on auditor tenure decisions in FTSE 100 firms” is researchable.

- Identify your research gap. Read recent journal articles in your chosen area and ask what questions remain unanswered.

- Choose a feasible methodology. Consider whether you will use qualitative interviews, quantitative data, case studies, or document analysis. Your method must suit your research question.

- Align with current academic standards. In 2026, examiners expect research that engages with current regulatory, ethical, and technological developments in the field.

- Plan your timeline. A dissertation is a long-term project. Set milestones for each chapter and stick to them.

For students who find the proposal stage particularly challenging, accessing professional auditing research assistance early in the process can prevent delays and improve the quality of your initial submission.

Conclusion

Auditing is a discipline that demands rigour, critical thinking, and a genuine engagement with real-world financial and ethical issues. Choosing a strong dissertation topic is the foundation on which all of that work rests.

This post has outlined 80 contemporary auditing research topics, provided five structured examples of how dissertation topics are written with research aims and objectives, and explained the key subfields students can explore in 2026. Whether your interest lies in forensic auditing, compliance auditing, digital transformation, or audit ethics, there is a topic here that fits your academic level and research ambitions.

The most important thing you can do at this stage is begin. Read widely, narrow your focus, and commit to a question that genuinely interests you. The best dissertations are always driven by curiosity and a desire to contribute something meaningful to the field.

If you need further guidance at any stage of this journey, whether at the topic selection stage, the proposal stage, or during the writing process itself, academic support is available to help you move forward with confidence and integrity.